WHICH INSURANCE TYPE IS RIGHT FOR YOU?

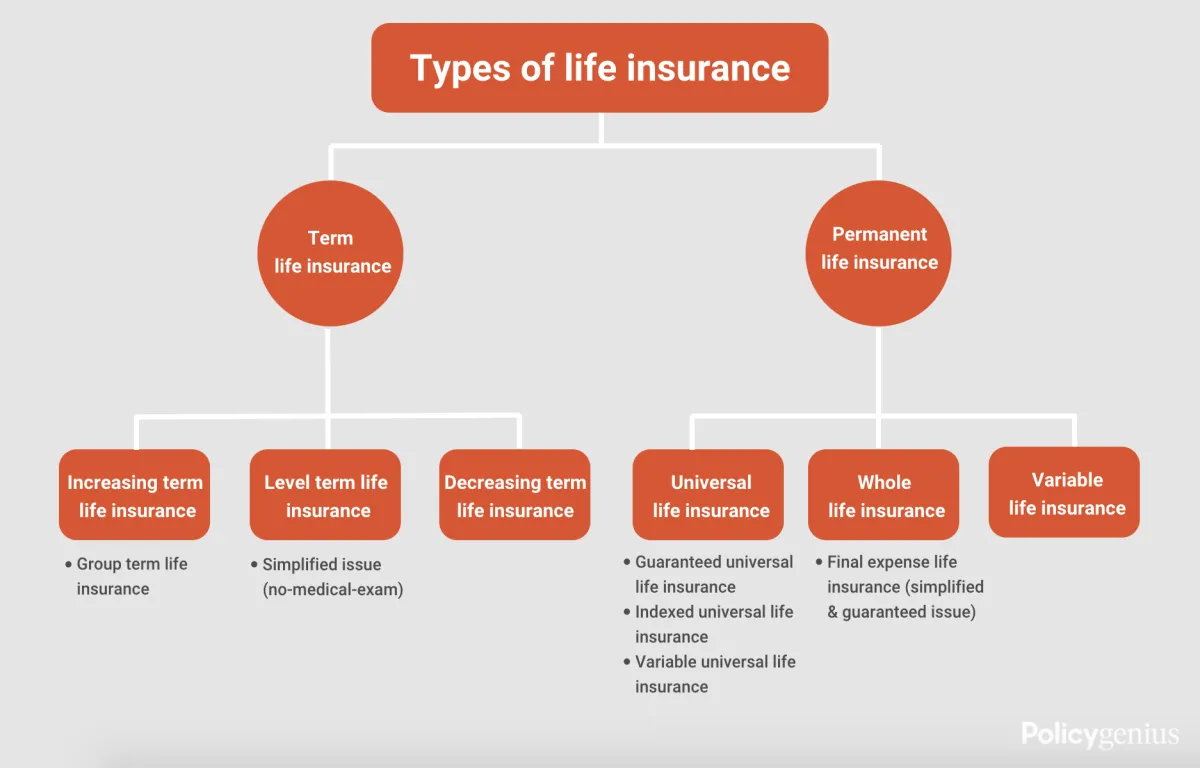

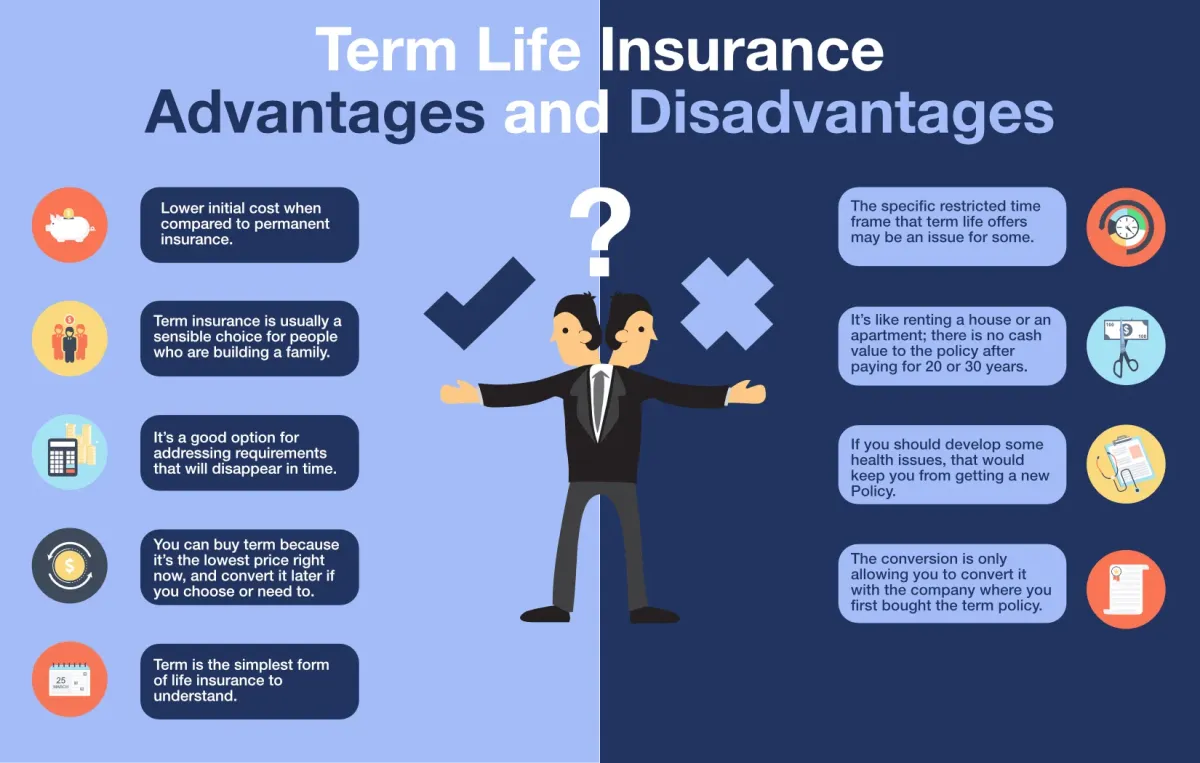

Types of Life Insurance Term Life Insurance Term life insurance is a type of life insurance that provides coverage for a specified term, usually ranging from 1 to 30 years. If the policyholder dies during the term of the policy, the death benefit will be paid to the beneficiaries tax-free. If the policyholder does not die during the term, the policy will simply expire without any value. Term life insurance is generally the most affordable type of life insurance and is best for individuals who want coverage for a specific period of time, such as to cover a mortgage or provide for dependents during their working years. Whole life Insurances

Whole life insurance, also known as permanent life insurance, is a type of life insurance that provides coverage for the policyholder's entire life. Unlike term life insurance, which only provides coverage for a specified term, whole life insurance does not have a set expiration date. It provides a death benefit for the policyholder's beneficiaries and also has a cash value component that accumulates over time, allowing the policyholder to build savings. Whole life insurance generally has higher premiums than term life insurance, but it provides a more comprehensive coverage solution with a lifelong death benefit and a potential source of savings. Whole life insurance is best for individuals who want a permanent life insurance solution and the potential to build long-term savings. Juvenile Life Insurance

Juvenile life insurance: Juvenile life insurance policies generally have low coverage amounts, but they can be a great way to start building a financial safety net for a child's future. The premiums for juvenile life insurance policies are generally lower than those for adult policies and may stay level for the duration of the policy, regardless of the policyholder's age. Some juvenile life insurance policies also have a savings component that allows the policyholder to accumulate funds for future expenses such as education or retirement. Juvenile life insurance can be a good option for parents or grandparents who want to provide a financial safety net for their loved ones and secure their financial future.

Indexed Universal Life (IUL): IUL insurance is a type of permanent life insurance that combines the death benefit protection of traditional whole life insurance with the potential for cash value growth tied to market indexes such as the S&P 500. The cash value growth of an IUL policy is tied to the performance of a market index, but with a cap on the maximum amount of growth that can be achieved. Some carriers offer guaranteed minimum interest rates. This provides policyholders with the potential for higher returns than traditional whole life insurance while also limiting their downside risk (typically 0%). IUL policies also typically have flexible premium payments and death benefit options, allowing policyholders to tailor the policy to meet their individual needs and goals. IUL is best for individuals who want a permanent life insurance solution with the potential for higher returns on their cash value and the ability to customize the policy to meet their specific needs and goals.

Who Needs Life Insurance?

Everyone should use good insurance planning to prepare for more than just replacing a lost income. Life insurance can provide for future needs of your family or business.

Individual/Family Needs

Funeral – Provide the funds needed for a proper funeral and burial expenses.

Estate Taxes – Preserve the value of your estate by using life insurance funds to cover federal estate and state inheritance taxes.

Mortgage Protection – Pay off the balance of a mortgage or provide an income stream to pay monthly mortgage or rent payments.

Income Replacement – Provide a supplemental income stream to ensure that your surviving family members are able to maintain the same standard of living.

Debt – Cover personal loans, credit cards, student loans and other debts. Future Education – Ensure that the education costs of your children are covered.

Charitable Donations and Gifts – Fund a donation to a charity or a gift to a family member.

Business Needs

Key-Employee Protection – Protect against the financial loss to your company from the unexpected death of a key employee.

Business Continuation – Fund a buy/sell agreement plan to arrange for the orderly transfer of your business at your death, disability or retirement by using life insurance policies with either death benefits or cash values.

Executive Benefits – Build an attractive benefits package for selected employees by paying premiums for life insurance.

Salary Continuation/Deferred Compensation – Provide supplementary income to selected key employees and their families in the event of the death, disability or retirement of the key employee.

Whatever your need for life insurance, that need can change over time. At any age, you should consider your individual circumstances and the standard of living you wish to maintain for your dependents.

All rights reserved. This is not an offer to enter into an agreement. Information and programs are subject to change without notice.

Brennan Senior Insurance

Thomas Brennan

59 Camelot Drive, Farmingdale NJ 07727

brennant09@gmail.com

(732) 614-9848

custom_values.company_logo=https://storage.googleapis.com/msgsndr/c2el4U0gPevCuOfPxhZm/media/6584c502805e6e0093319443.png

custom_values.headshot=https://storage.googleapis.com/msgsndr/c2el4U0gPevCuOfPxhZm/media/6584c502805e6e0093319443.png